May, 18, 2026

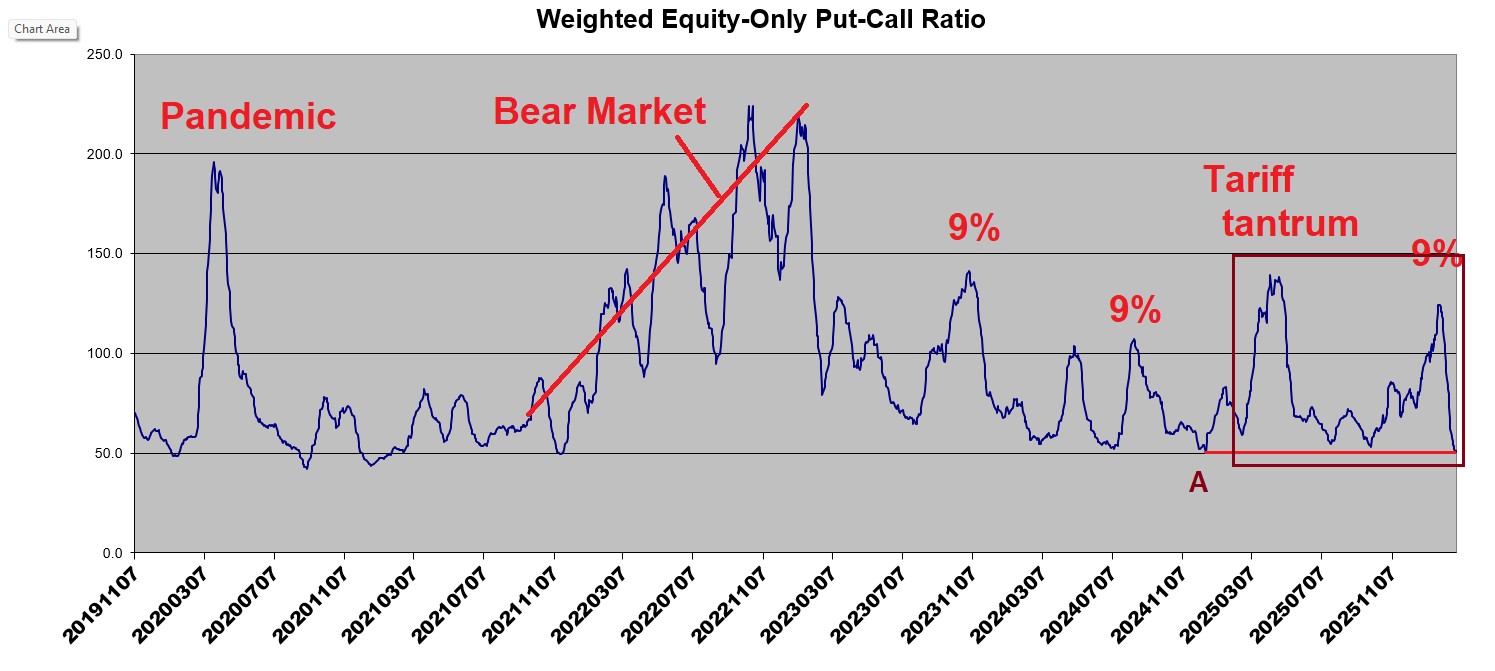

By Lawrence G. McMillanWith euphoria abounding in the stock market, call buying has been rampant. That has forced the put-call ratios to drop precipitously. The weighted ratio is at a multi-year low...

May, 15, 2026

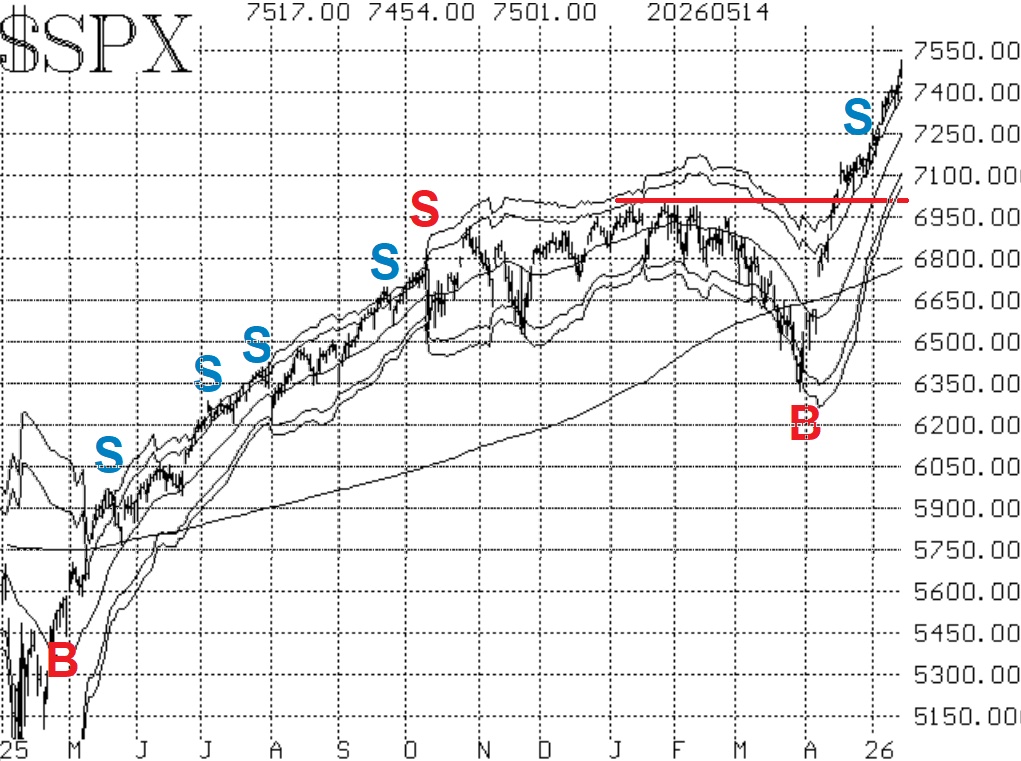

By Lawrence G. McMillan$SPX continues to surge, having made new all-time highs on four or the last five trading days. There is minor support at 7338 (the past week's low), and at 7275 (the bottom of...

May, 12, 2026

By Lawrence G. McMillanJoin Larry McMillan as he discusses the current state of the stock market on May 11, 2026.

May, 08, 2026

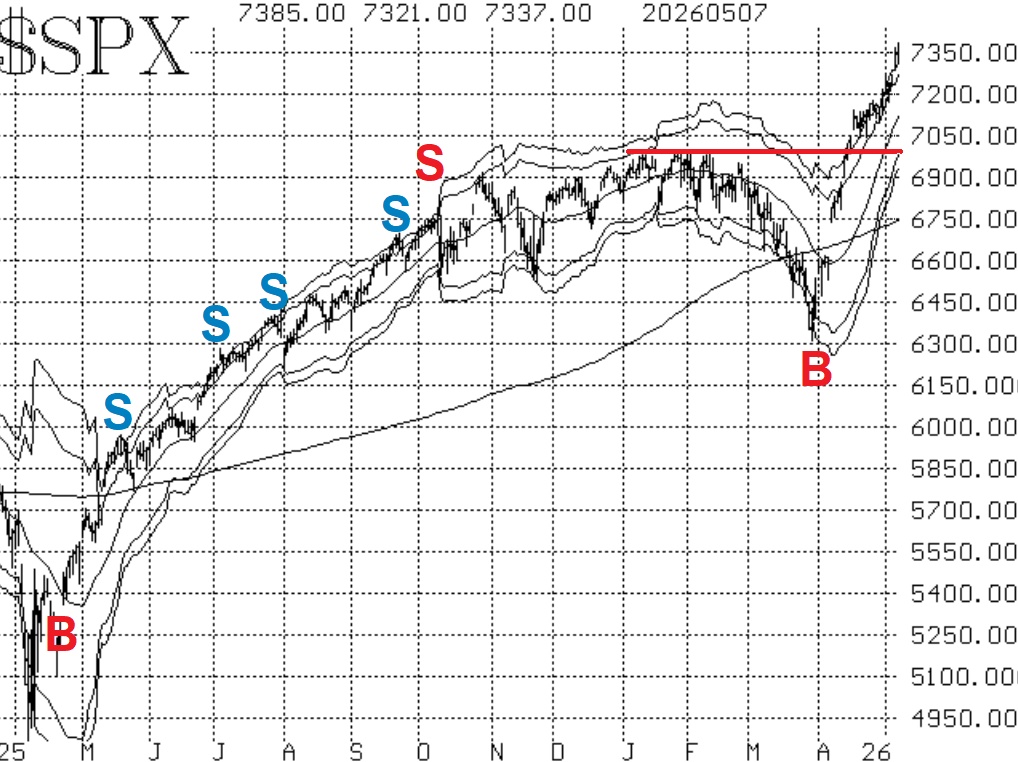

By Lawrence G. McMillanWhether you think it's MOMO (momentum) or FOMO (Fear Of Missing Out), or whatever, it doesn't really matter. This market is a perfect example of why "overbought does not mean...

May, 04, 2026

By Lawrence G. McMillanJoin Larry McMillan as he discusses the current state of the stock market on May 4, 2026.

May, 01, 2026

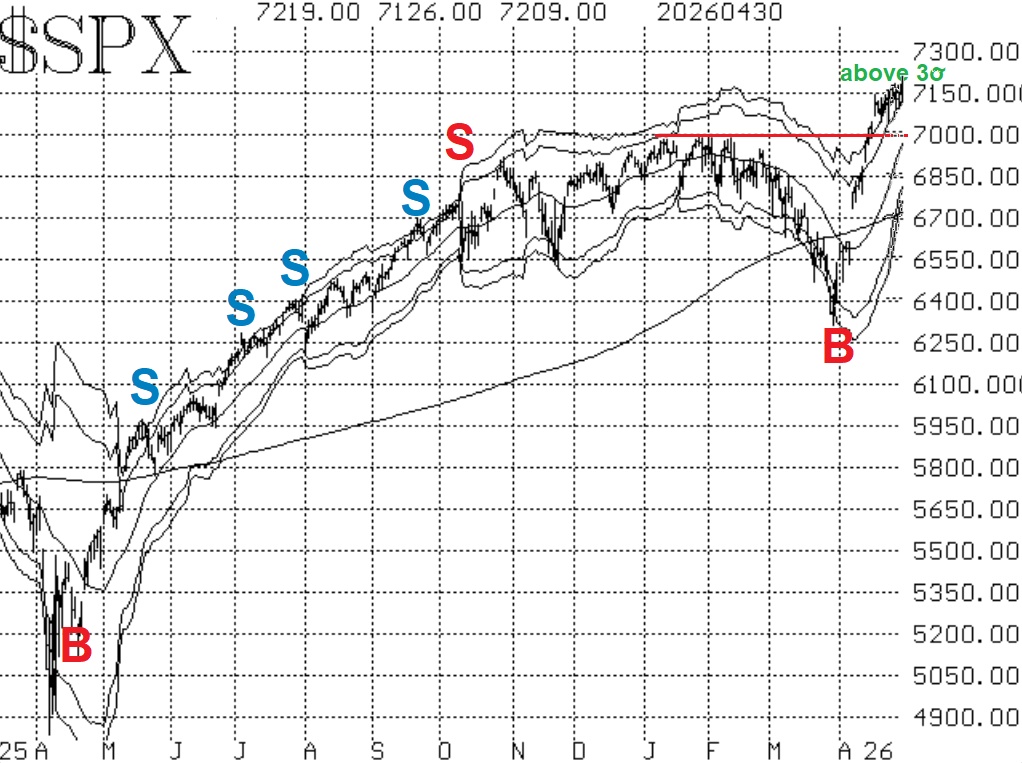

By Lawrence G. McMillanThe major indices are all enjoying a booming bull move to new all- time highs $SPX, $NDX, and $RUT (while the Dow is closing in on its highs as well). This display of strength...

May, 01, 2026

By Lawrence G. McMillanSome traders prefer to see columns of numbers, and others—myself included—prefer to look at graphs or charts. A “profit graph” is a graph of the potential profits and losses...

Apr, 27, 2026

By Lawrence G. McMillanJoin Larry McMillan as he discusses the current state of the stock market on April 27, 2026.

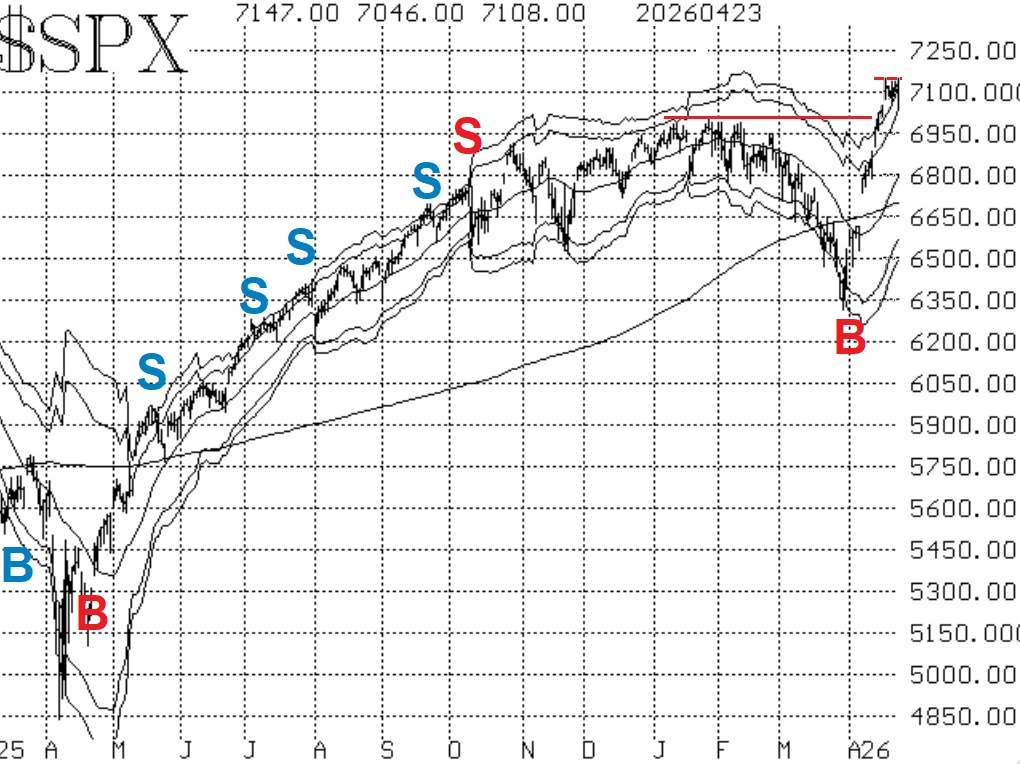

Apr, 24, 2026

By Lawrence G. McMillanThere are two major approaches to analyzing markets—technical and fundamental. Most investors are familiar with fundamental analysis. That is the process by which analysts...

Apr, 24, 2026

By Lawrence G. McMillanSeveral of the major indices ($SPX, $NDX, and $RUT) have made and held new all-time high ground recently. Pullbacks have been small, and it appears that there is still an...

Pages

© 2023 The Option Strategist | McMillan Analysis Corporation