By Lawrence G. McMillan

One of things I’ll always remember about the Crash of ‘87 (actually, I’ll always remember everything about the Crash of ‘87 – at least from my vantage point) was that the market was down on Wednesday, Thursday, and Friday of the week before, with Friday being the worst day. That Friday, October 16th, saw the Dow drop 110 points – the largest point drop in history up to that time. Of course, Monday was the Crash. On that Monday, the futures opened down about 20 points (roughly equivalent to 120 points today, by my estimate). So I learned to respect a market as being potentially extremely bearish if there is a big drop into a closing low on Friday. Another notable (bad) memory came in August, 2015, when $SPX opened down 100 points on Monday after an ugly close to the week before.

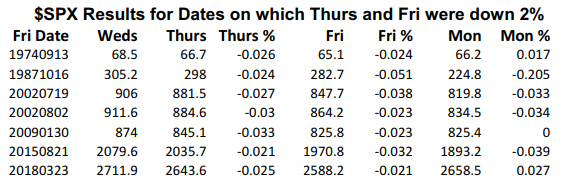

Some research out of Schaeffer Investment Research last week pointed out that on the six previous occasions that the market had closed down at least 2% on Thursday and 2% on Friday, it was higher a week later, except for the Crash of ‘87. Well, yes, but you could be run over in the meantime. In that August 2015 situation, the market opened down 100 points on Monday. Yes, it closed the week with a gain of a couple of points, but you probably had been stopped out for a big loss if you bought on Friday, and the market was crashing on Monday.

This past week, for the second time in the now seven occurrences of -2% moves on both Thursday and Friday, the market was up on Monday (the other was October 1974, and while I was trading then, I don’t remember that move specifically).

But whether up or down, the six occurrences that don’t include the Crash of ‘87 saw a 2.5% move, on average on Monday. So, it seems to me that buying a straddle on that Friday close is probably the best strategy. Moreover, since it is likely that the front-month $VIX futures would be trading at a big discount on that Friday close, the ultimate strategy would be: buy “the market” and buy “volatility” – our VXX/SPY call hedge. The complete data is in the table below.

Some further notes: the 1974, July 2002, and 2009 occurrences were during a heavy bear market – even near the ends of those bear markets. 1987, Aug 2002, 2015, and 2018 were not ongoing bear markets at the time they occurred, although $SPX was off its highs by the time these moves happened.

What If Only Friday is Down Big?

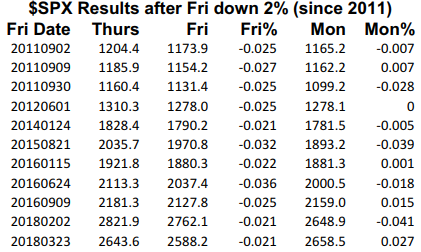

In a related manner, on Friday, February 2nd, of this year, $SPX was down by 2.1%. Then, on Monday, it collapsed 4.1%. So I wanted to see if a Friday collapse alone of 2% was significant. There have been 65 such occurrences since 1950. And it’s almost a coin flip as to how Monday after a 2% down Friday is going to turn out. There have been 32 Mondays that were higher, 31 that were lower, and 2 that were unchanged. Furthermore, the median move is literally 0%. The average move is –0.6%, but that’s because the Crash of ‘87 throws a huge number in there on the minus sides (-20.4%).

Whether up or down, the absolute value of the average move is 1.8% – again, worth buying a straddle or setting up the VXX/SPY call hedge. But wait! 1987 is skewing that. The median move is 0.9%. That’s not necessarily going to produce a profit, especially if options’ implied volatility is pumped up on Friday’s close after the big down day.

I would have thought that such a negative Friday move would carry over into more selling on Monday. But the statistics don’t agree. Moreover, it’s not really clear that a “neutral” strategy would profit, either. I suppose you have to look at things on a case-by-case basis. If the options are not overly expensive, or if there is a large discount on the front-month $VIX futures, then the hedged strategy might make sense. Otherwise, probably not.

Just FYI, the following table shows the most recent “down 2+% Fridays:”

Five of the last six have been sizeable moves (although two are duplicates from the above table).

In summary, it’s likely worth investigating the VXX/SPY hedge on Friday’s close when these set up.

This article was originally published in the 3/29/18 edition of The Option Strategist Newsletter.

© 2023 The Option Strategist | McMillan Analysis Corporation