By Lawrence G. McMillan

This has been a successful seasonal trade in many years, and last year was the second best year in our history. We have used this in 22 of the past 23 years – skipping only 1995, for reasons which I no longer recall.

In this trade, we buy RBOB Gasoline futures and sell Heating Oil futures. This is the simplest way to establish the spread, eschewing futures options and ETF options – the options are just too illiquid in the February contracts, which is what we use for this spread.

Figure 5 shows a composite of this spread over the past 25 years. The optimal entry is 56 trading days after the end of August – which this year is Friday, November 18th. The optimal exit date is in early January, but in reality we trade this with a trailing stop, and usually exit a bit earlier than that.

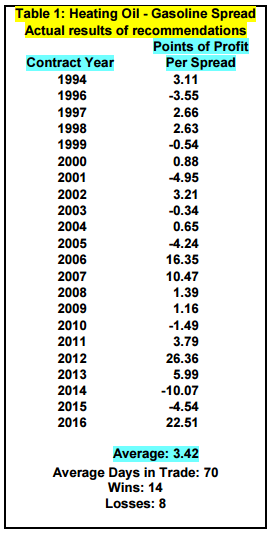

Table 4 shows the yearly results that we have actually experienced in our trades, having traded 22 times in the past. The Year shown in the table is the year of the futures contracts, not the year when the trade was established, so for example, the 2016 line in the table was last year’s trade, using contracts that expired in February 2016...

Read the full feature article (published 11/11/16) by subscribing to The Option Strategist Newsletter.

© 2023 The Option Strategist | McMillan Analysis Corporation