By Lawrence G. McMillan

One of the questions that traders – both retail and professional – have been asking all throughout the bear market that began in January 2022 is “What Is Wrong With $VIX?” Everyone remembers the $VIX explosions during the crisis events over the years, but there is little memory of $VIX seemingly ignoring a bear market decline such as the 25% that has occurred in this bear market. In reality, there have been similar declines with a non-responsive $VIX before, but it is just not something that stands out in one’s memory like the upward spikes do. In this paper, we’ll look at some of those past occurrences and see if we can discern if there is indeed anything wrong with $VIX or not.

The Behavior of Realized Volatility in Bearish Markets

First, let’s set $VIX aside and just concentrate on how the realized volatility of the stock market behaves during bear markets. In short, long but rather steady declines see only a modest increase in realized volatility, while sudden declines – even crashes – tend to see an explosion in realized volatility.

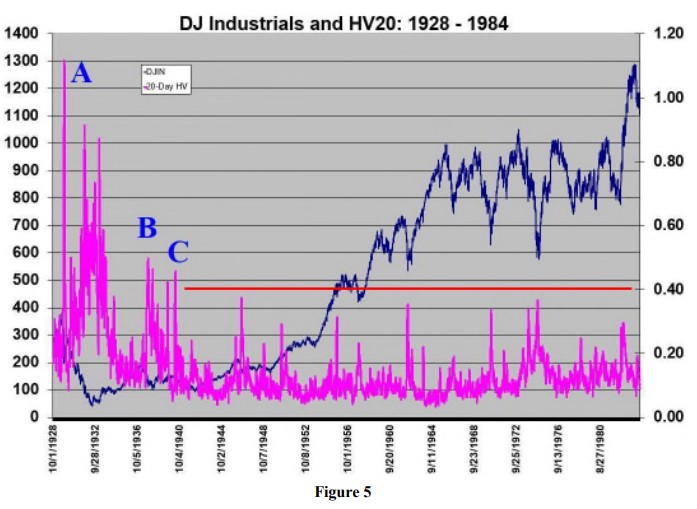

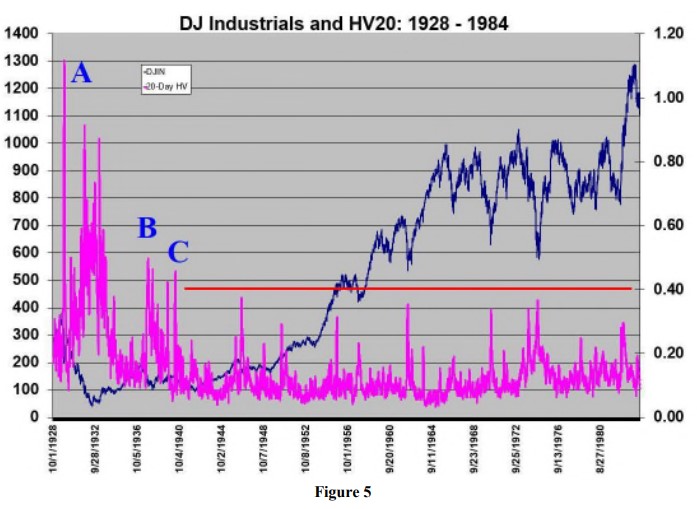

Figures 5 and 6 show realized volatility1 in the form of the 20-day historical volatility, going back into the 1920's. These two figures use the Dow Jones Industrials as the “stock market,” because the S&P 500 was not widely popular for most of these time periods. The scale of the Dow is on the left, and the Realized Volatility (20HV: 20-day historical volatility) uses the right-hand scale. In this paper, “realized volatility” and “20-day Historical Volatility” are synonymous terms, unless stated otherwise.

Figure 5 encompasses 1928 to 1984. On the far left is the Crash of 1929 and the subsequent Great Depression (point A in Figure 5). Prices were extremely volatile during this period because not only was the market crashing and/or dropping extremely rapidly, but also because the market got to a very low price (at the bottom in 1932, the Dow got down to 40). Lower-priced entities have higher realized volatilities than higher-priced ones do. Realized volatility was above 90% on three different occasions during that period.

Read the full article, published on 3/24/2023, by subscribing to The Option Strategist Newsletter now. Existing subscribers can access the article here.

© 2023 The Option Strategist | McMillan Analysis Corporation