By Lawrence G. McMillan

We are currently, in March 2020, in one of the three most volatile markets in history. In terms of absolute price change, it has no peers. In terms of percentage price change, 1929, 1931-1933, and 1987 are all in the mix (but not 2008, which has been surpassed). If we looked back even farther, there would be other markets which were volatile, too (1907, for example), but in this paper we are not looking back past 1928.

Overview

We begin by looking at the history of the Dow Jones Industrials, from 1928 to today, along with its 20-day historic volatility. We can’t look at implied volatility for much of that time, since options weren’t traded until the creation of the CBOE in 1973, and $VIX (the CBOE’s Implied Volatility Index) wasn’t created until 1993 (although it was back-dated to 1986). We will, however, look at the implied volatility history that we do have, for it is important as well. Only the last two volatility explosions – 2008 and 2020 – occurred while volatility derivatives existed, and we will incorporate those in our study as well.

Historic Volatility

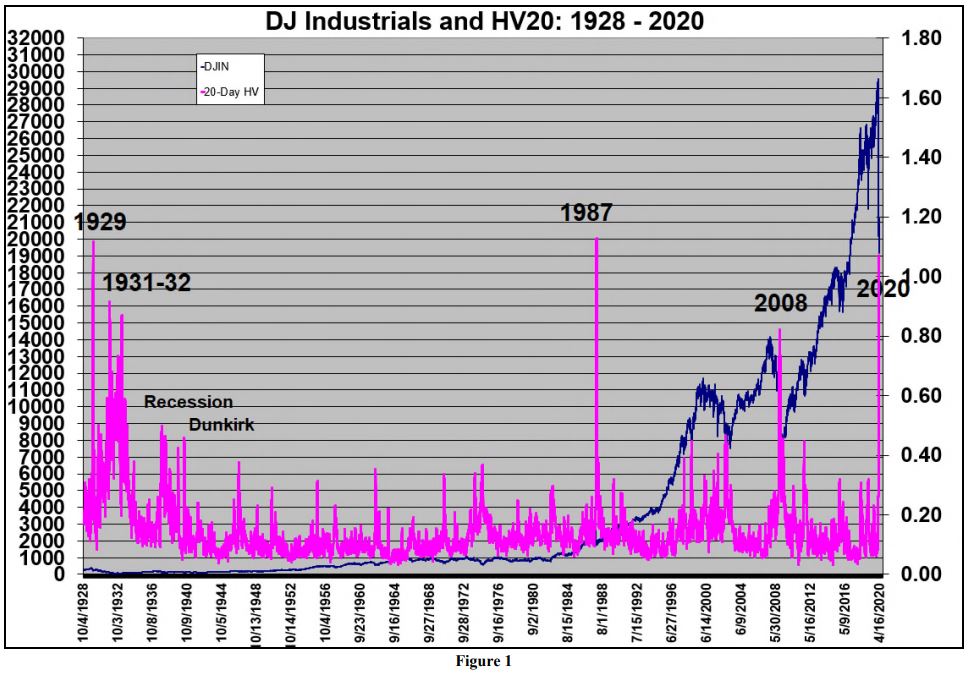

In Figure 1, we show the Dow Jones 30 Industrials (blue line) as well as its 20-day Historical Volatility (HV). This chart incorporates data from 1928 to the present. As of March 27th, 2020, the 20-day historical volatility of the Dow is 106%! This is one logical reason why $VIX is remaining at high levels above 60: because realized volatility is even higher than that.

You can see from Figure 1 that the volatility of the current market is on a par with the Crash of ‘87 and the Crash of 1929. Those were both short-term affairs, compared to the current market, but the damage inflicted has been similar....

Read the full article, published on 3/30/2020, by subscribing to The Option Strategist Newsletter now.

© 2023 The Option Strategist | McMillan Analysis Corporation