By Lawrence G. McMillan

The CBOE introduced the Volatility Index ($VIX) in 1993. The calculation of $VIX has changed a couple of times over the years, and due to the complexity of those calculations, $VIX itself cannot be traded. However, in 2004, $VIX futures were listed, and in 2006, $VIX options were listed. $VIX futures are the underlying instrument for all of the Volatility ETN’s and ETF’s that exist today (VXX, for example).

There is a lot of information in the $VIX futures – primarily in their relationship to $VIX (discounts or premiums) and in their relationship to each other (the term structure). We use those two things to determine the “construct” of volatility derivatives – a stock market indicator that we track in our general Market Commentary in our newsletters. But in this article, we’re not concerned with stock market predicting as much as we are in trading the market.

What is The Term Structure and Why Does It Slope?

The term structure of the $VIX futures refers to the price relationship that the futures have with one another. For example, an upward-sloping term structure generally occurs during a bullish stock market. The nearest-term futures would be the lowest-priced, then the second month futures would be slightly higher-priced, and the third month higher than both, etc.

The reason that the term structure slopes upward in bullish times has nothing to do with the futures market attempting to predict implied volatility. In fact, it’s really just the opposite: due to the vagaries of attempting to predict where long-term volatility is going to be, market makers will price longest-term $VIX futures somewhere near the average of long-term volatility. But in a bullish market, volatility is low, so the near-term futures will be trading with a volatility that is below average.

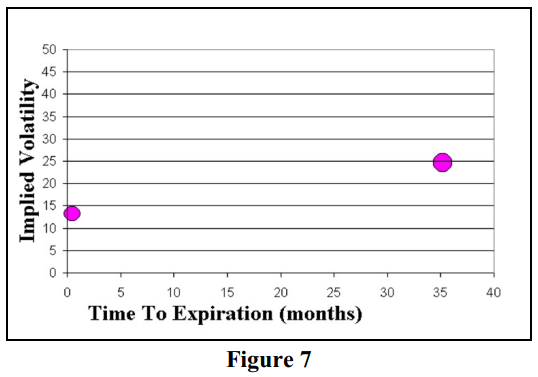

Consider an option buyer who approaches a market maker and asks “At what implied volatility would you sell me a 3-year option?” Since the market maker has no idea where volatility will be in three years, he will price it an average long-term volatility – say 25% in this case. Then the option buyer says, “At what implied volatility would you sell me a 1-week option?” Supposing that the stock market is bullish, and near-term implied volatility ($VIX) is 13, the market maker will price the near-term option with a 13 volatility. These two implied volatility points are shown in Figure 1. Futures at those time frames would reflect the same volatilities...

Read the full article, published on 8/16/2019, by subscribing to The Option Strategist Newsletter now.

© 2023 The Option Strategist | McMillan Analysis Corporation