By Lawrence G. McMillan

Last year (2018) was a very interesting year in a number of respects. One of those was the behavior of volatility and especially the behavior of volatility derivatives. Since one cannot trade $VIX but must instead trade one of the listed products – $VIX futures, Volatility ETN’s or ETF’s, or options on those instruments – there are some nuances involved. Since all of those instruments are based on $VIX futures1 , that is where we’ll concentrate this discussion.

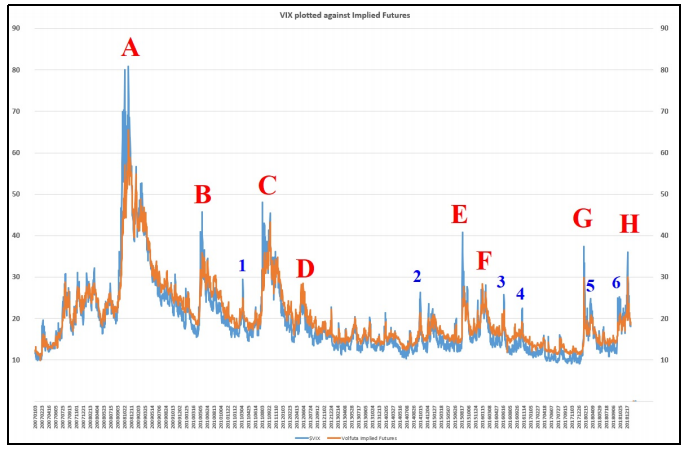

We know that $VIX futures have subdued moves in comparison to $VIX. When $VIX drops to extremely low levels, the futures do not follow – instead trading with some premium. That is the case during bullish stock market phases. But when the stock market drops and $VIX accelerates, $VIX futures don’t keep pace on the upside either. They trade at discounts to $VIX. Just how much of a discount they trade at is unclear. At some times in the past, the discount has been huge and at other times, minimal. That’s what makes it difficult to predict just how effective a long position in volatility derivatives will do during a stock market collapse. In a true crisis – a la October 2008 – a long volatility position made a lot of money just due to the pure size of the increase in $VIX futures; discount be damned. But in a less severe market decline, which can still be very painful for those long the market, the discount on the $VIX futures does matter...

Read the full article, published on 1/18/2019, by subscribing to The Option Strategist Newsletter now.

© 2023 The Option Strategist | McMillan Analysis Corporation