By Lawrence G. McMillan

As it stands today, the “Short Volatility Trade” has been watered down to a great extent. Perhaps in an effort to get ahead of the regulators, most of the Exchange Traded Products (ETPs) that deal with “short volatility” have made adjustments so that their products are no longer as volatile as they had previously been.

While there are several short volatility ETPs in existence, only three have the trading volume to be viable: SVXY (the ProShares short volatility ETF), VMIN (the REX VOLMAXX short volatility ETN), and ZIV (the Credit Suisse intermediate-term “brother” of the now-defunct XIV). These all have reasonable liquidity now that XIV is gone. There are a few others that we will discuss later in this article.

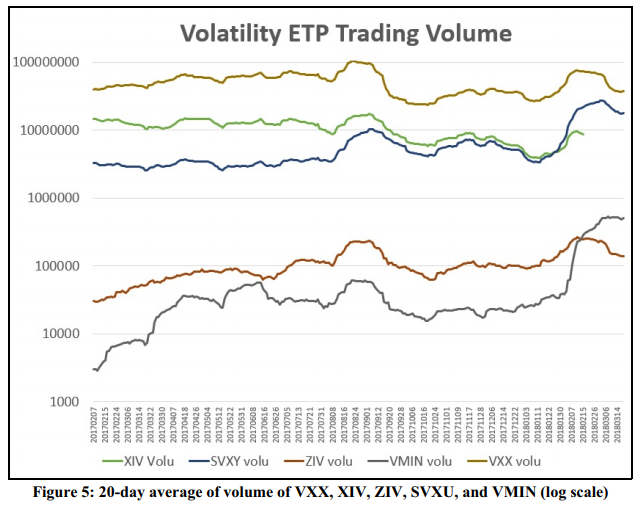

Figure 5 shows the 20-day average volume of five Volatility ETPs, charted on a lognormal scale. The five are the four short volatility ETPs noted above and the major “long volatility” ETN – Barclay’s VXX, which was the first volatility ETN listed – back in late January, 2009. It was necessary to use lognormal because VXX volume is so dominant that the least active ones would be dwarfed on a linearly-scaled chart. The chart covers the time period from January 2017 to March 2018. In January 2017, from highest volume to lowest, they lines on the graph are VXX, XIV (no longer trading), SVXY, ZIV, and VMIN.

There was a surge in trading volume of all of these ETPs in August, 2017, during a very small market correction. The recent stock market decline, which began in late January 2018 has increased volume in SVXY and VMIN past those peaks of last August, as they have picked up some of the volume that had previously been trading XIV. ZIV volume is tapering off after a brief post-XIV surge. VXX remains the most active, but ironically it was more active last summer than it is now. I say “ironically” because VXX is arguably a better “long volatility” now than it was then, because the $VIX futures are trading with small premiums or discounts, and the term structure of the $VIX futures is relatively flat; both of these factors are beneficial to the price of VXX.

In addition to VXX, there are a lot of “long volatility” ETPs. VIXY (Proshares VIX short-term Volatility ETF) is one that is rather liquid. Two of the more prominent leveraged volatility products are UVXY (the Credit Suisse “ultra long volatility” ETF) and TVIX (the “double speed long volatility” ETN, issued by VelocityShares).

The “short volatility” trade made a lot of money from January 2009 through January 2018 – particularly in 2017, when the market marched steadily upward as volatility languished. For a full recounting of the trade and its sudden demise in February of 2018, please refer to our article “XIV – the scapegoat of the market’s decline,” published in our newsletter of February 16, 2018.

For a while, the short volatility trade was taking the primary blame for the market’s sudden collapse, even though the market was already declining rapidly before the short volatility ETPs imploded (in fact, that’s why they imploded; if the market hadn’t already been declining – causing volatility to explode – there wouldn’t have been a problem in the first place). There were, of course, other reasons why the stock market collapsed and still hasn’t recovered. Witness the fact that almost every other sector (bonds, gold, currencies) has struggled as well. The short volatility trade certainly didn’t affect them. Regardless, there was a hue and cry from uninformed but vocal critics in the media, and apparently there was some concern among the underwriters of the short volatility products that perhaps they were too volatile for the “average investor” – or at least, that might be a legal argument brought against them.

This seems to me to be a ridiculous argument. The main problem was that a few investors had not bothered to read the prospectuses or did not believe them. The prospectuses clearly spelled out the dangers if the underlying $VIX futures were to explode by more than 100% in a day – something that is certainly possible in a crashing stock market. These people would not have been protected even if the products had been less volatile.

Adjustments to Volatility ETPs

Let’s see how these adjustments have been made, and how they will affect the ETPs going forward. The first adjustment to be made was by ProShares (well perhaps the first adjustment was by Credit Suisse, when they terminated XIV). ProShares reduced the leverage on the short volatility ETF, SVXY to one half of its former status. In other words, it only moves half as fast as the blended $VIX futures do. With that adjustment, it would take a 200% increase by the underlying $VIX futures to wipe out SVXY – not the 100% increase that formerly was in effect. While it is certainly true that it is more difficult for the $VIX futures to increase 200% in one day than to increase 100%, it is still possible. Even though $VIX did not exist during the Crash of ‘87, the CBOE later estimated that it would have increased from under 30 to about 150 on that day. The $VIX futures wouldn’t keep pace with a move of that size, but they would certainly have increased more than 200%.

Meanwhile, this adjustment to SVXY means that traders who understand the risks and are willing to accept them, now have to deal with a much slower-moving vehicle when trying to short volatility. I would surmise that a great deal of them will look for another product to use.

Proshares didn’t just water down SVXY, they also did it to their “ultra long volatility” product, UVXY. Previously UVXY had been designed to move at twice the speed of $VIX futures. Hence, it could have lost all of its value had $VIX futures fallen by 50% in one day (since UVXY moved at double-speed, that would have been a loss of 100% for UVXY). Now the multiplier has been reduced to 1.5. So it would take a 67% decline by those $VIX futures to wipe out UVXY (67% times 1.5 = 100%, roughly). So, yes, there’s a smaller chance of a total wipeout happening, but most traders in UVXY are there for the upside leverage. Besides, since there are options on UVXY, one can always hedge himself with those.

Before addressing the next two ETN’s, let’s pause for a bit of a refresher on how volatility behaves. A very short-term product (say, an $SPX option) will have a volatility that reflects the current volatility of the underlying – in this case, $VIX, since it is based on the implied volatility of options on the S&P 500 Index. However, a long-term option will have a rather static volatility – something near the long-term average volatility of options on $SPX. At time intervals in between, the volatilities are relative: shorter-term options will have volatilities that move more in accordance with $VIX, while longer-term options’ implied volatilities won’t change much at all. For a more in-depth discussion of this topic, see the article “Some Comments On The $VIX Futures Term Structure” in the issue published on March 31, 2017, and a follow-on article the next week.

We have often stated that if one is attempting to simulate the movements of $VIX , he should stay with short-term products. One cannot trade $VIX itself, but can only trade the derivative products related to $VIX. This necessity to utilize short-term $VIX derivatives is especially true if one is buying volatility to protect a stock portfolio, but is also true if one is speculating on the direction of volatility. If one goes farther out in time – say using 3- or 4-month $VIX futures instead of short-term futures – he won’t get much movement out of those at all when $VIX makes a quick move. One startling example is what happened in September and October of 2008, after Lehman Brothers went out of business, and the market went into a severe nosedive. In one period of about three weeks, $VIX rose from 24 to 54. The nearest-term $VIX futures rose about 22 points – not as much as $VIX, but still a decent move if one owned them to protect his stocks. However, the Feb 2009 $VIX futures – about five months out in time – only rose 6 points. That would have been poor performance for both those desiring protection for their stocks and for those speculating on a rise in volatility.

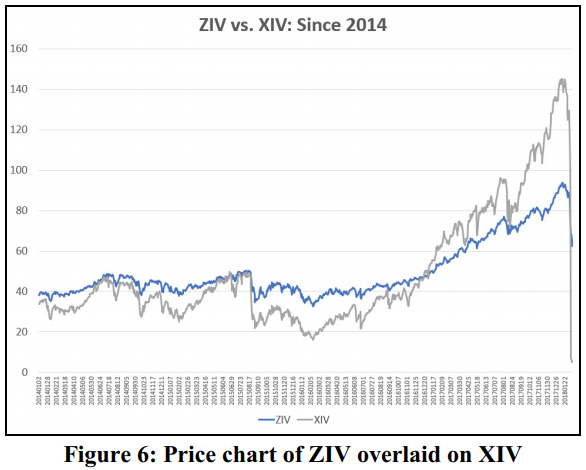

With that in mind, consider ZIV – the intermediate-term “short volatility” ETN. The graph in Figure 6 compares the movements of ZIV (which utilizes an average 5-month maturity of $VIX futures as its underlying) with XIV (which, prior to its demise, used the front two months). You can see that ZIV doesn’t move very swiftly at all, in comparison to XIV. All of the “intermediate-term” ETPs use $VIX futures of approximately those durations – 3 to 6 months. For that reason, most of the intermediate-term volatility ETPs don’t have much (open) interest at all. There just isn’t a lot of demand for slow moving volatility ETPs. So this really isn’t an attractive vehicle for sophisticated traders looking to short volatility.

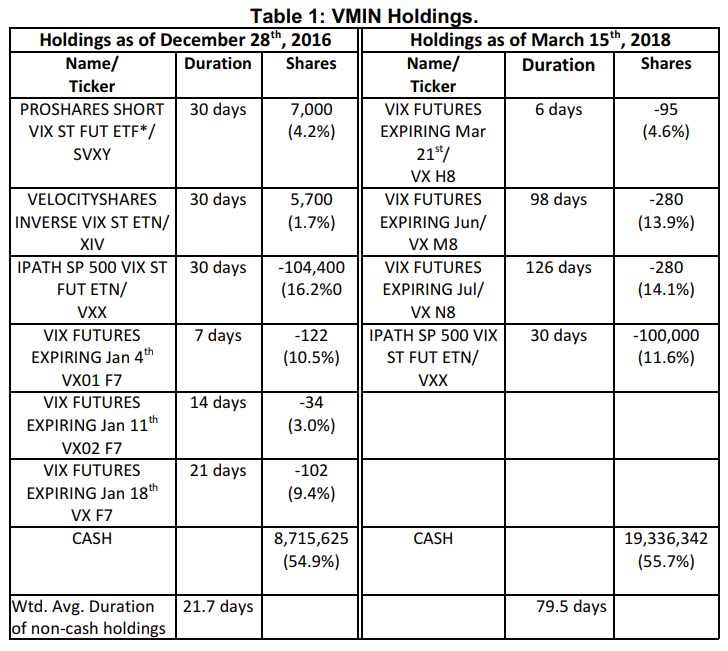

This then makes one wonder why in the world the operators of VMIN (the REX VOLMAXX increase volatility ETN) made the changes they did. When we first wrote about this product (the issue of December 30, 2016), we described it as “XIV on steroids.” It was designed to move fast and to maximize the short volatility effect. Now, apparently worried about the VMIN being able to move too fast, the underwriters have lengthened the average time to maturity. This essentially converts it to an intermediate-term short volatility product, which won’t have much movement at all.

Consider Table 1, which lists the holdings of VMIN. The first was from late 2016, when we initially wrote about the product. It was geared up with a lot of short-term products designed to profit if volatility declined (and to blow up if volatility exploded). There wasn’t any product longer than 30 days, and the average duration of the six short vol holdings was 21.7 days.

Compare that with the current holdings on the right side of the table. Currently, VMIN is short a few March futures and short 100,600 shares of VXX. It has no position in short ETP’s as it did before (SVXY and XIV). In addition, VMIN is short June and July futures in order to “lengthen” the maturity of the portfolio. The average duration of the March 15th holdings is 79.5 days – much, much longer than before. A duration of that length will not be very responsive to movements in $VIX. So what’s the point of owning this any longer?

I suppose that VMIN could once again shorten its time to maturity, but it’s unclear if they ever will. In a white paper, the company explains that “we can see that a basket with short exposure to the 3rd and 4th month contracts would have survived the extreme moves of February 5th with ‘only’ a ~50% downdraft, roughly speaking, a far less steep drop than for a basket composed of short position in the 1st and 2nrd month contracts.” That much is true, but do short vol traders want to minimize losses or maximize gains?

We have explained many times that if one is in these “short vol” products, he needs to exit when the term structure of the $VIX futures flattens. Frankly, he should probably exit if the term structure even gets to a very small upward slant. Using that guide, one would have been out of the short volatility ETPs on February 2nd or earlier – avoiding the devastation that followed. Hence, once can control the risk himself; he doesn’t need the designers of the products to do it for him.

Other Short Vol ETPs

In the course of doing the research for this article, I came across a couple of other short volatility products. Most are illiquid and are copies of already-existing products. But one that I found interesting was XIVH (The VelocityShares Short Volatility Hedged ETN). What made this at least a little different is that it is supposedly composed of 10% of a “double long” volatility position plus 90% of a short volatility position. Thus their target exposure is “70% short volatility.” In reality, the product may have a far different exposure; more about that shortly.

At the target exposure, the product would be worthless if “volatility” rose by 143% in a day. In that case, the 10% “double long” would make 28.6%, but the 90% short vol would lose 128.7%, and the product would be wiped out.

But the actual exposure to volatility changes daily, as the price of “volatility” changes and can become quite different than the stated target exposure. One thirteenth of the “holdings” are rebalanced weekly – rebalanced to the 70% short volatility exposure target. But if something crazy happens, it takes a long time for the rebalancing to get things back to where they need to be.

For example, consider the case of the huge explosion in volatility in early February of this year. The exposure was –70.16% on February 1st, right where it is targeted to be. On February 2nd, the stock market dropped sharply and volatility jumped sharply higher. That made the exposure only –57.65%. Then, on February 5th, when volatility rose 100%, the exposure completely flipped and this supposedly “short volatility” product actually had a long volatility exposure of +177.5%! That has dropped daily since then, and was about +50% on March 21st. You can check the daily exposure of XIVH on the web, at http://www.velocitysharesetns.com/xivh At the bottom of that web page is a circle that shows the long exposure and the short exposure.

This is interesting, but not particularly useful, for who would want to trade a product in which you are not sure what your volatility exposure is going to be from day to day?

Summary

In summary, the short vol trade will once again be viable, but only after the term structure of the $VIX futures begins to slope steeply upward once again. However, it is going to be far less profitable to play it with this current array of products. The only thing that hasn’t changed is VXX.

Since VXX has options, perhaps the best approach to shorting volatility is to buy puts or put spreads on VXX. We have been using VXX puts to implement the “Big (Volatility) Short” strategy for several years. ■

1Credit Suisse made the decision to terminate XIV after the debacle that occurred when it lost nearly all of its value in a single day, on February 5, 2018. It was within their rights to do so, even though it wasn’t actually necessary since the ETN still had net asset value above 0.

This article was originally published in the 3/23/18 edition of The Option Strategist Newsletter.

© 2023 The Option Strategist | McMillan Analysis Corporation