By Lawrence G. McMillan

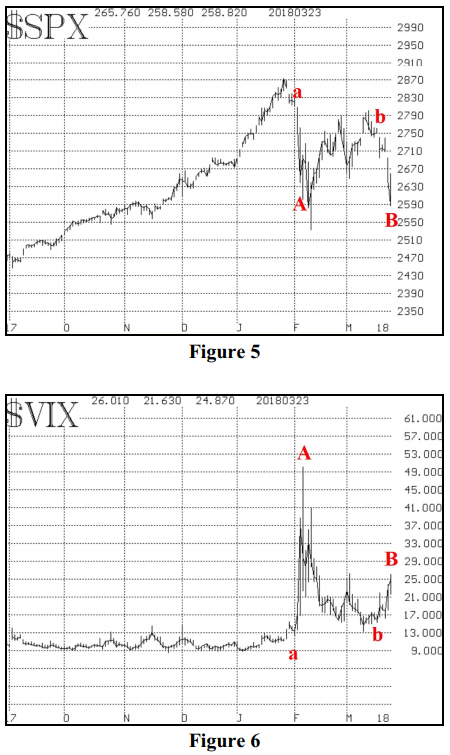

Last week we published an article showing the different reactions of $VIX to the initial 6% drop in the stock market in early February, as compared to the 6% drop in the stock market in March. In February, $VIX exploded from essentially 15 to 50. In March, a similarly-sized move in the stock market only produced a rise in $VIX from about 15 to 25. That’s a big difference. For reference, those reactions are shown in Figures 5 and 6 – reprinted from the last issue.

There has been much speculation as to why this occurred, and much of it has no way of being proven right or wrong – such as “everyone already owns all the protection they need, so they aren’t burying any more.”

There has been much speculation as to why this occurred, and much of it has no way of being proven right or wrong – such as “everyone already owns all the protection they need, so they aren’t burying any more.”

What I thought might be interesting, though, is to look at an extended period of increased volatility to see if this is a “normal” occurrence or if it’s unusual this time. Obviously the first such period that comes to mind is the 2007-2009 bear market. That one was so extreme that one cannot expect the volatility patterns there to be repeated until the next financial crisis, which could be decades away. (For the record, volatility exploded on the first sharp market drop in August 2007, didn’t pull back to its lows even though $SPX made new highs in October 2007, and was generally higher for a year or so – with spikes when new $SPX lows were made – until the massive volatility explosion in September-October 2008)...

Read the full article by subscribing to The Option Strategist Newsletter.

© 2023 The Option Strategist | McMillan Analysis Corporation